Mapping Deposit Pathways: Mobile Loyalty Structures Accelerating User Advancement

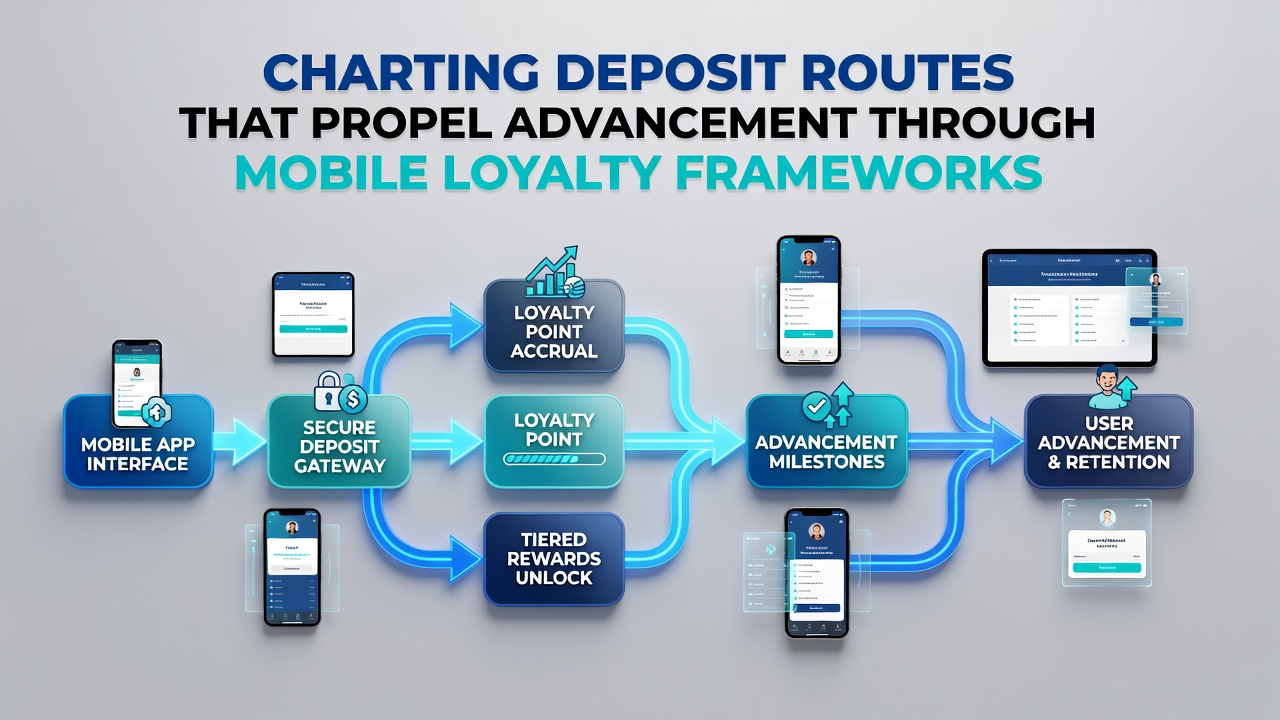

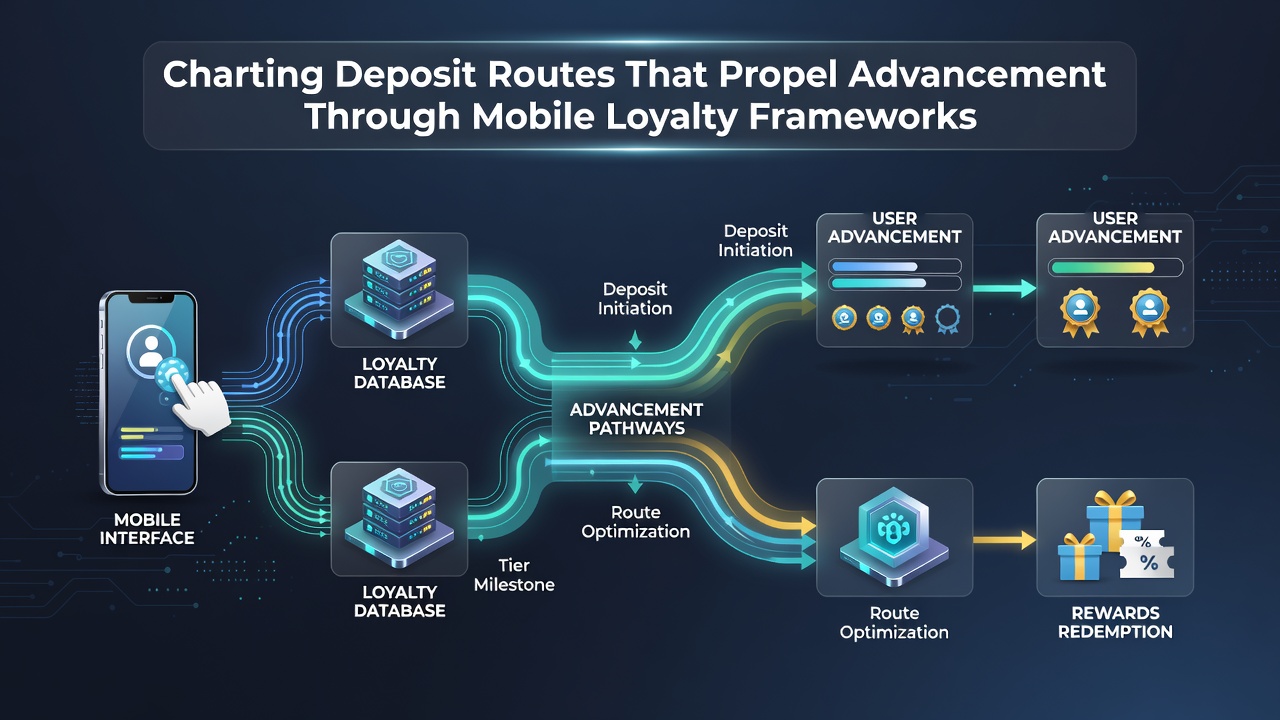

Digital platforms have developed intricate systems where deposit routes serve as foundational elements within mobile loyalty frameworks, and these pathways allow users to progress through structured reward tiers based on consistent funding activities. Observers note that such frameworks integrate payment processing with engagement metrics so that each deposit not only credits an account but also triggers advancement protocols designed to retain participation over extended periods.

Payment methods range from bank transfers and digital wallets to card-based options, while each route carries distinct processing times and verification requirements that influence how quickly users unlock subsequent levels. Research from the OECD indicates that streamlined deposit integration correlates with higher retention rates across various mobile service sectors, and data collected through 2025 showed continued expansion into automated reconciliation tools that reduce friction during initial funding steps.

Core Components of Deposit Integration

Mobile loyalty frameworks rely on several interconnected elements that convert deposits into measurable progress indicators, and these include tier thresholds, multiplier bonuses for repeated activity, and real-time tracking dashboards visible within the app interface. When users select a deposit route, the system evaluates factors such as amount, frequency, and payment source before assigning points or status upgrades, which then determine access to exclusive features or enhanced reward rates.

Those who have studied these mechanisms report that automated verification layers now operate in tandem with loyalty algorithms, and this coordination minimizes delays between deposit confirmation and reward allocation. In July 2026, several platforms introduced enhanced API connections that further synchronized banking partners with loyalty engines, resulting in near-instant progression updates for verified users.

Progression Mechanics and Route Selection

Users typically begin at entry-level tiers where modest deposit amounts establish baseline activity records, yet repeated engagement through preferred routes can accelerate movement toward mid-tier and premium categories. Data shows that frameworks offering multiple deposit options, including recurring scheduled transfers, tend to produce steadier advancement patterns compared with one-time funding methods alone.

Take one regional banking application that implemented route-specific incentives during early 2026, where direct payroll deposits earned additional multipliers toward status elevation, and participants who maintained consistent monthly funding reached higher reward brackets within shorter timeframes. Such examples illustrate how route selection directly shapes the pace of advancement within the overall loyalty architecture.

Industry Data and Adoption Patterns

Figures released by the Mobile Marketing Association reveal that loyalty-integrated deposit systems appeared in over 65 percent of top-ranked financial and retail applications by the second quarter of 2026, and these implementations often featured dynamic routing that suggested optimal payment channels based on user history. European and North American platforms demonstrated parallel growth in adoption, whereas Asia-Pacific markets emphasized integration with local instant payment networks that reduced settlement times.

Studies conducted at academic institutions, including work published through the University of Melbourne's digital economy research unit, found that transparent route mapping increased user comprehension of how deposits translated into loyalty benefits. Participants exposed to visual progress indicators completed more funding actions per month on average, which in turn supported sustained framework engagement.

Security and Compliance Considerations

Regulatory bodies in multiple jurisdictions have issued guidelines requiring clear disclosure of how deposit data feeds into loyalty calculations, and compliance frameworks now mandate audit trails that document each route's contribution to tier progression. Financial technology providers have responded by embedding encryption protocols and consent mechanisms directly into the deposit flow, ensuring that users retain control over which payment sources connect to their loyalty profiles.

What's interesting is the emergence of cross-border route compatibility, where users traveling between regions can maintain continuity of advancement through standardized verification partnerships. Industry organizations such as the Global System for Mobile Communications Association have documented these developments in recent technical briefs, noting that interoperability standards continue to evolve in response to user demand for seamless international access.

Future Trajectory Through 2026 and Beyond

Platform developers continue refining algorithms that predict optimal deposit timing and amounts for individual users, and these predictive tools aim to balance reward distribution with sustainable business models. Observers note that integration with emerging authentication technologies, including biometric confirmations, has further reduced barriers associated with route initiation while maintaining compliance with data protection requirements across different markets.

Evidence suggests that continued investment in route visualization tools will remain a priority, as clearer mapping helps users understand the connection between their funding choices and long-term advancement opportunities within mobile loyalty environments.

Conclusion

Deposit routes function as essential conduits within mobile loyalty frameworks, converting routine funding actions into structured pathways for user advancement across digital platforms. As systems mature through 2026, the emphasis on transparent integration, security standards, and adaptive routing continues to shape how participants navigate reward structures and achieve progressive status levels based on consistent engagement patterns.